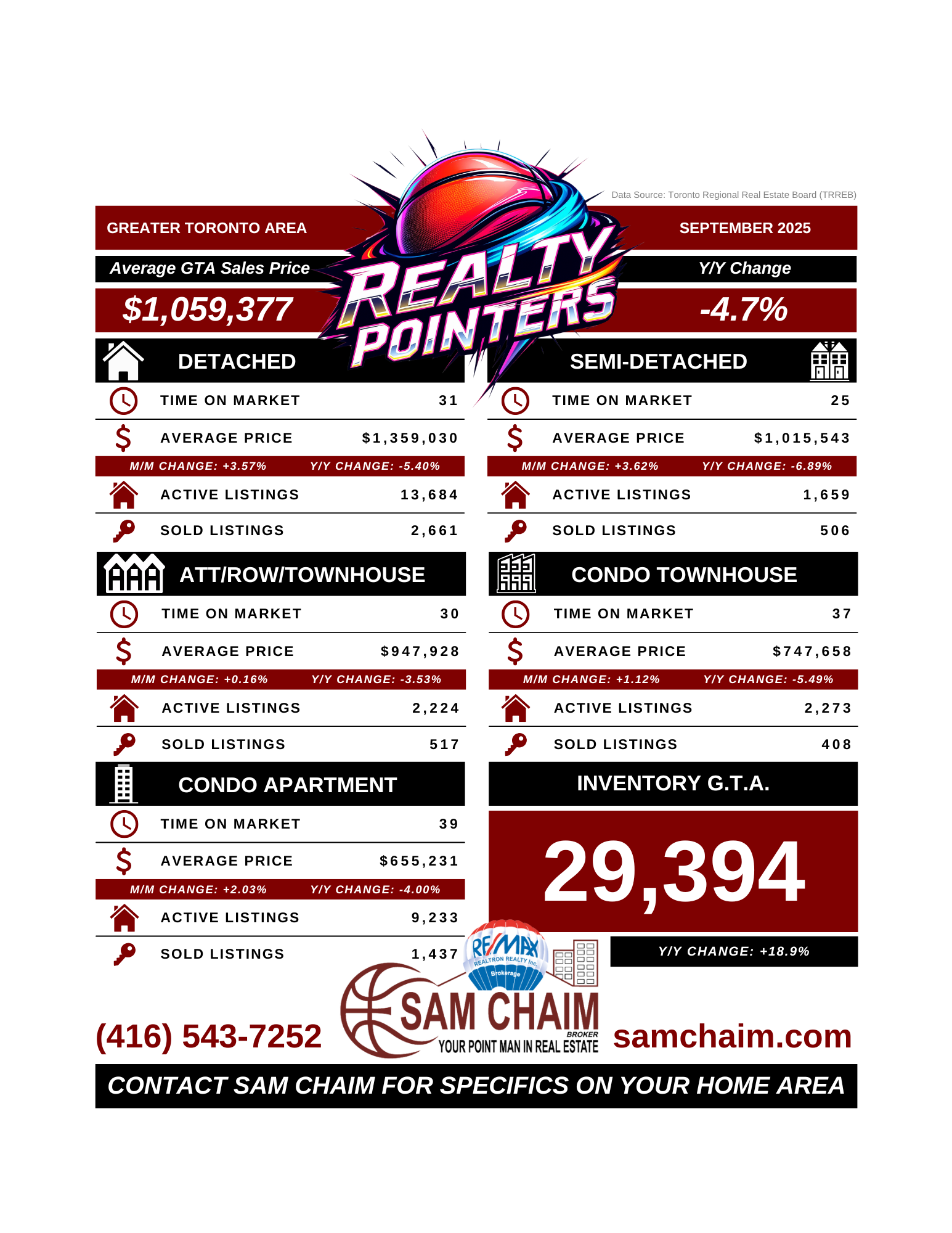

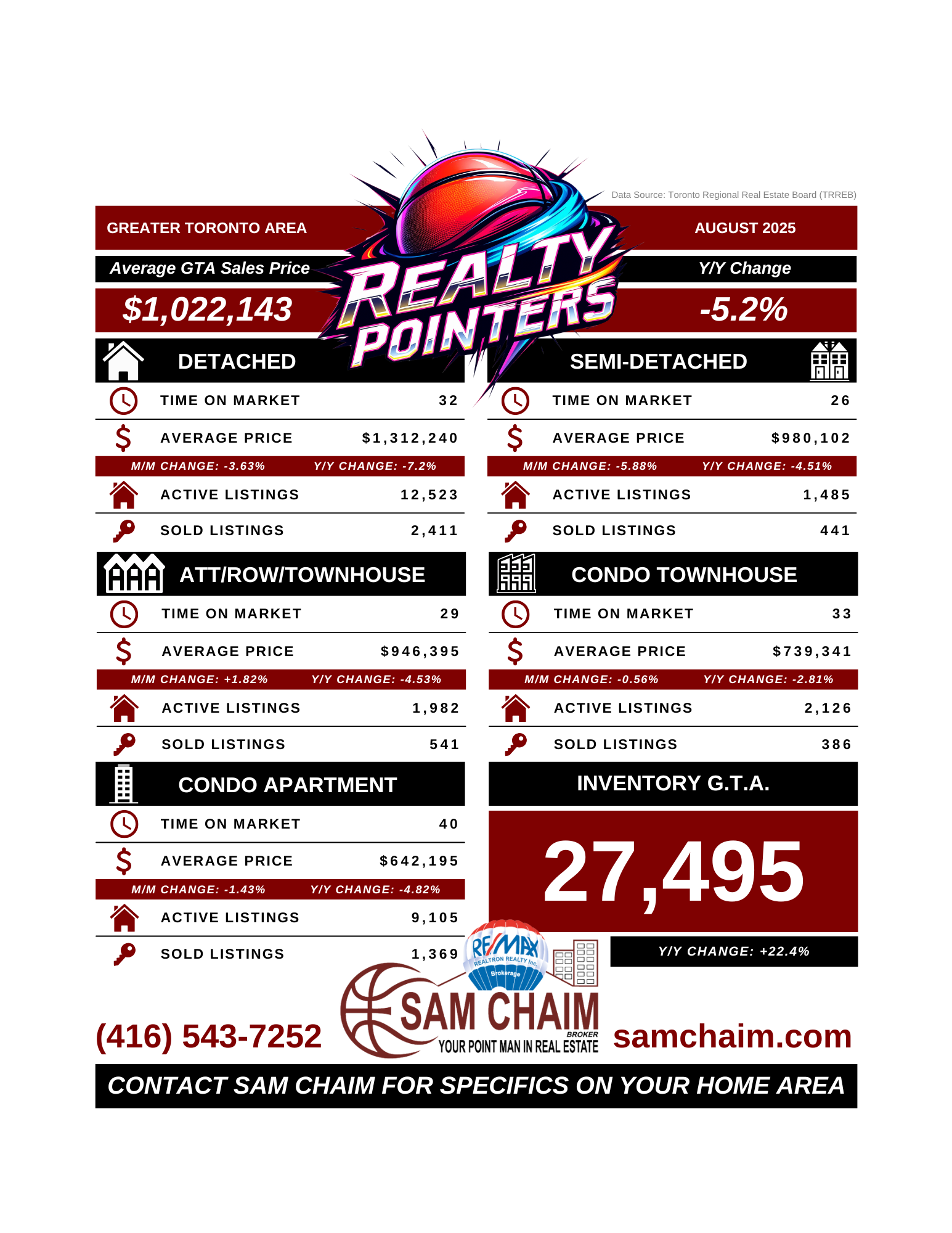

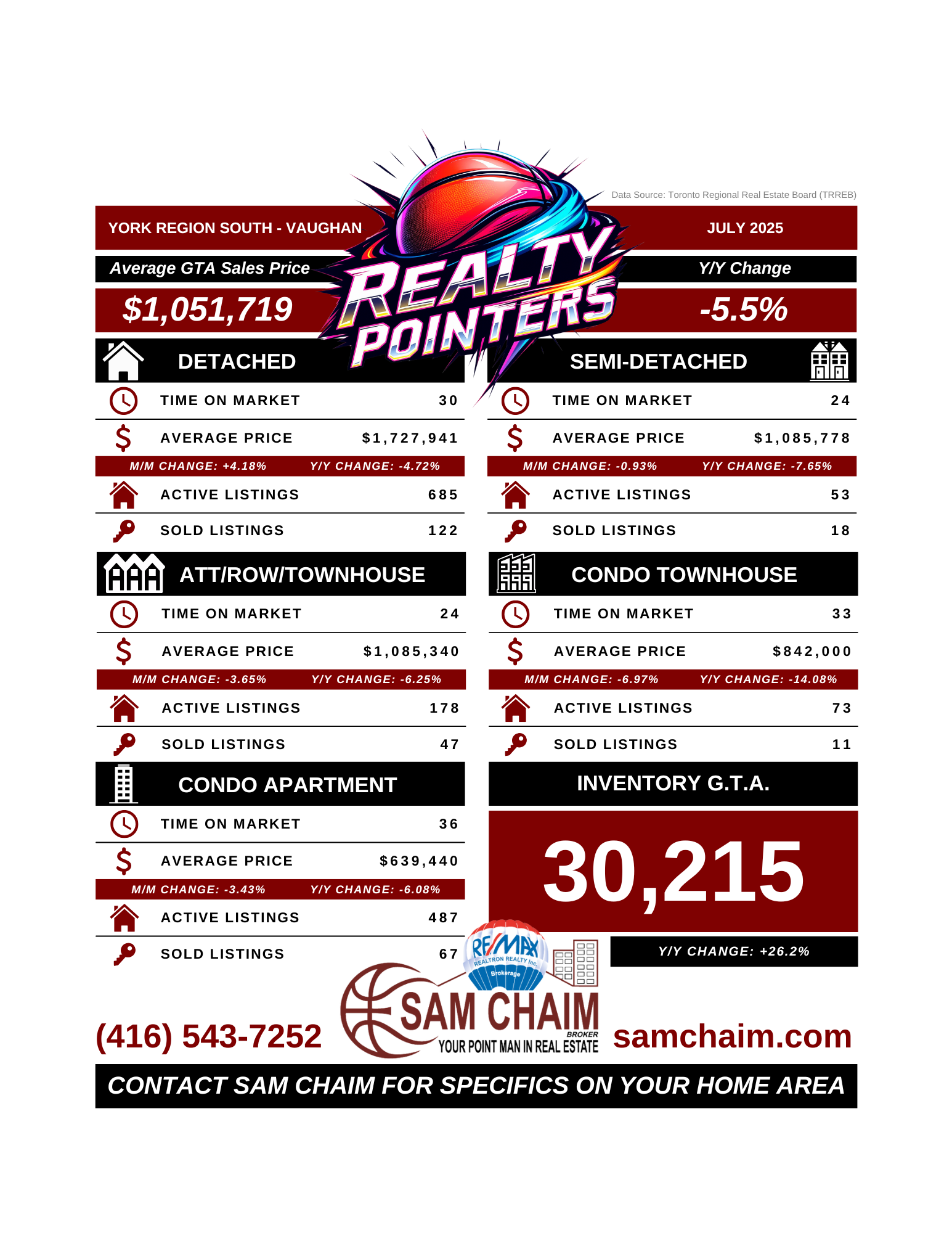

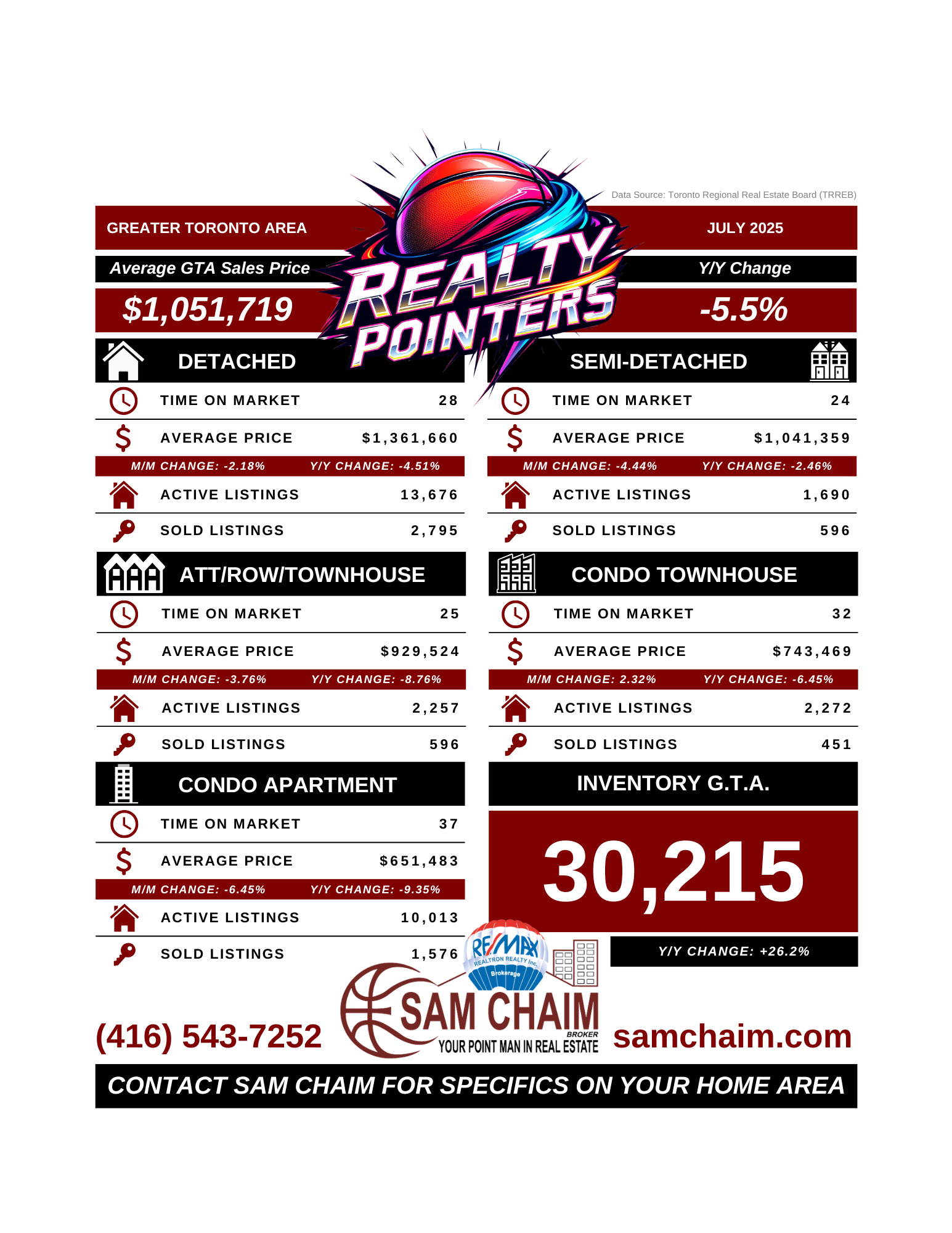

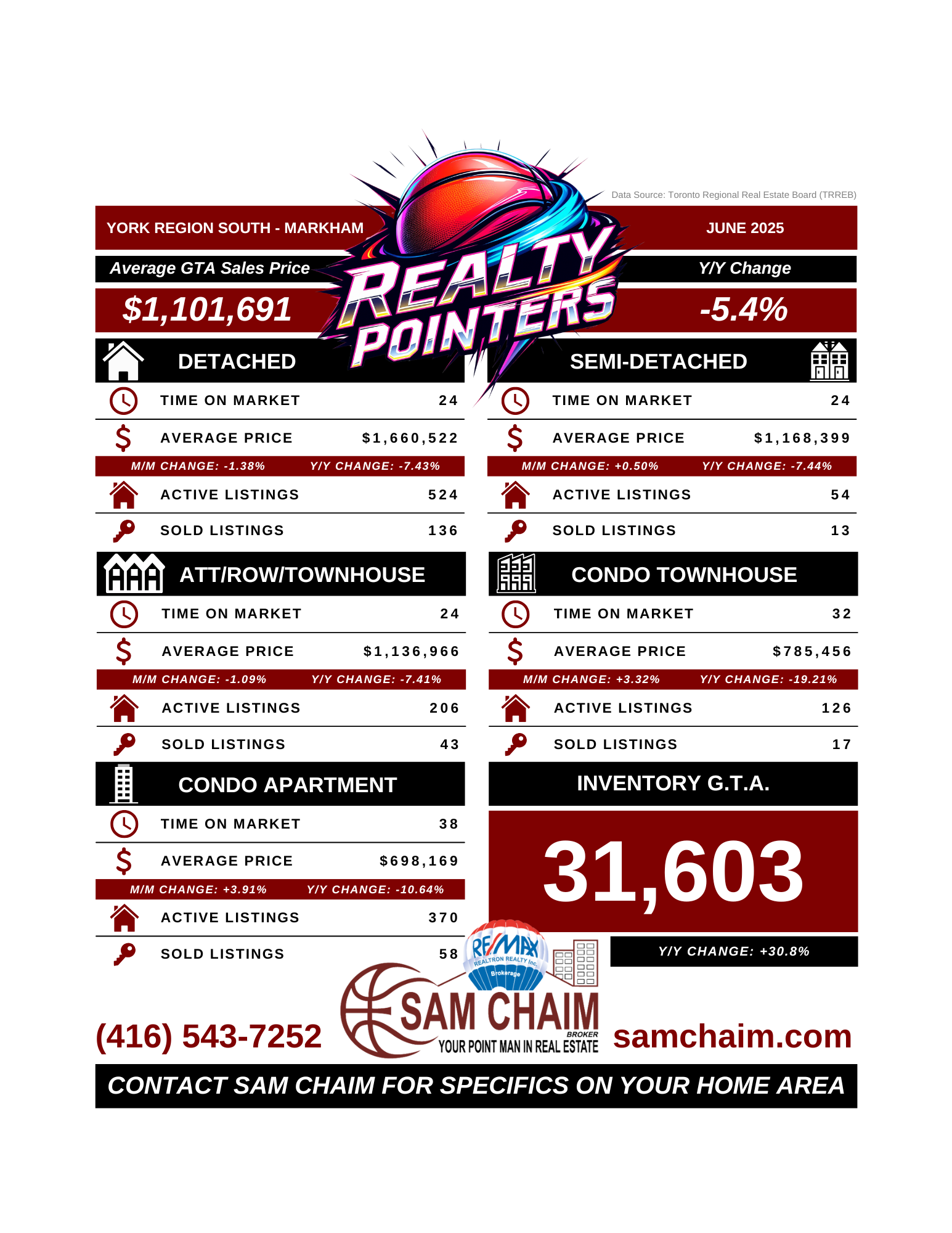

The October 2025 Toronto Regional Real Estate Board numbers highlight meaningful changes across the Greater Toronto Area housing market — changes that matter whether you’re considering selling, buying, or investing.

Average GTA Home Price: $1,054,372

The average selling price is showing a 7.2% year-over-year decline, while overall inventory has increased 17.2%. More supply and more negotiability mean buyers have regained leverage — but strategic sellers are still achieving strong results.

Detached Market

Average Price: $1,355,506

Time on Market: 29 days

Active Listings: 12,879

Detached homes continue to lead the market, but success depends on competitive pricing and polished presentation.

Semi-Detached Market

Average Price: $1,033,770

Time on Market: 23 days

Semi-detached properties remain attractive to buyers seeking value while staying close to central neighbourhoods.

Townhomes & Condo Townhomes

Townhome Average Price: $935,042

Condo Townhome Average Price: $735,123

Townhomes and condo townhomes continue to be strong entry points for buyers and investors, benefiting from lower borrowing costs and improved affordability.

Condo Apartments

Average Price: $660,208

Time on Market: 39 days

Condos remain the most accessible segment and continue to draw investor attention.

What Sellers Need to Know

In a buyer-leaning market, pricing precision, professional marketing, and strong negotiation are essential. Well-prepared listings continue to perform — but strategy is everything.

What Buyers & Investors Should Watch

With lower monthly carrying costs, more inventory, and greater flexibility at the negotiation table, this market is creating opportunities not seen in recent years.

Whether you're planning to list your home, purchase, or explore investment opportunities, I’m here to help you make confident decisions.

To A Good Life,

Sam